Supply of commercial space

Overview of commercial space supply and marketability

The supply of commercial space refers to undeveloped, commercially usable areas that are legally represented in land use plans (F-Plan) or development plans (B-Plan). This includes

- Commercial (G) and mixed development areas (M) in the land use plan (F-Plan) and industrial estate (GE),

- restricted commercial area (GE-e),

- industrial area (GI),

- restricted industrial area (GI-e),

- mixed-use area (MI),

- core area (MK) or

- Special area (SO with various earmarking: large-scale retail, hotel/sport/leisure, science/research, medical university or airport expansion) according to BauNVO.

A legally valid B-plan (usually developed from the F-plan) and existing development are required for building rights. If there is already a concrete interest in use, the F-plan amendment and B-plan preparation are often carried out in parallel.

On the other hand, in some cases, B-plan preparation decisions are made, but the procedure is then not pursued further - often for years - because, for example, a prospective user has postponed his or her project. The time it takes to mobilize B-plan and F-plan areas can therefore vary greatly depending on the individual case.

In addition to the legal force of the B-plan, the status of the development and the municipality's accessibility via municipal ownership or a municipal project development are also decisive for the marketability or availability of the land.

In the following, the availability of commercial space is divided into four categories (Fig. 7; Tab. 2):

- B-plan, immediately marketable: Areas with a legally valid B-plan, existing development and in public ownership. In total, 55 ha of commercial land in the Hannover Region are to be classified as immediately marketable in 2024. The figure has therefore increased compared to 2023 (45 ha).

- B-plan, later marketable: Areas with a legally binding B-plan that have not yet been developed and/or are not publicly owned. At 150 ha, this area volume has also increased compared to the previous year (126 ha).

- F-plan: Areas for which an F-plan designation exists but not yet a legally binding B-plan and for which there is generally no development. Here, the municipality documents its basic planning objective as part of the preparatory urban land-use planning. However, it remains to be seen whether and when these areas will actually receive building rights through binding urban land-use planning (legally binding land-use plan, development). The majority of these areas are privately owned. At 446 ha, the amount of F-Plan land has decreased slightly compared to the previous year (451 ha).

- Potentially reusable brownfield sites: Due to generally considerable restrictions on use (e.g. old buildings that can no longer be used, contaminated sites, inadequate urban land-use planning), these areas have the lowest level of marketability. At 86 ha, the volume of brownfield land is slightly below that of the previous year (88 ha).

- The municipalities are currently discussing preview areas (intended new designation of commercial areas without B-plan or F-plan designation) in the order of approx. 518 ha. According to a survey of the municipalities, around 10 ha of these preview areas could currently be converted into building rights in the short term and 130 ha in the medium term.

The following chart illustrates the development of the total supply of commercial space - including potentially reusable brownfield sites as of 2015. Within the last ten years, the supply has decreased by 22 % (Fig. 7).

When looking at the total supply, it should be noted that potential land without a legally binding development plan will be significantly reduced in the course of the planning process due to areas for development and public green spaces, among other things.

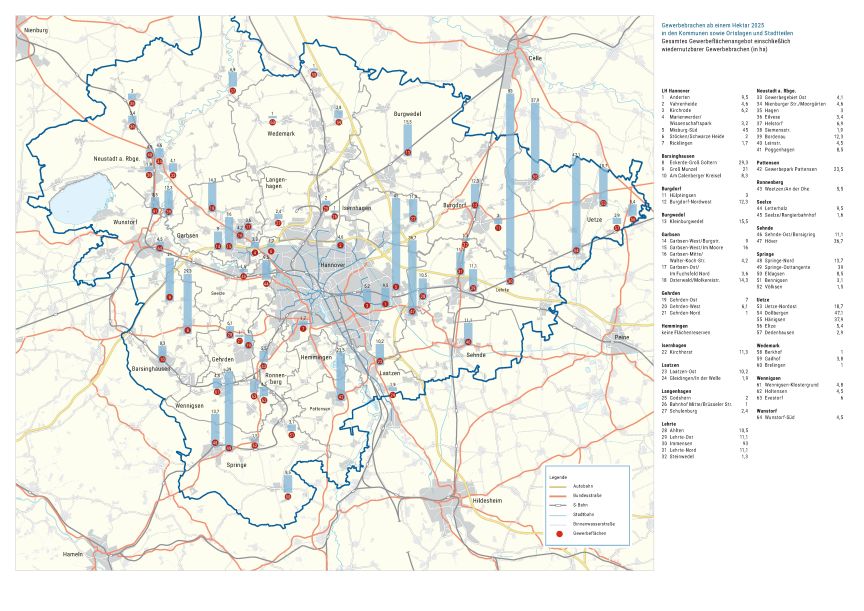

Table 2 shows the distribution of the current supply of commercial space across the respective municipalities:

- Larger potential areas of immediately marketable B-plan sites (> 5 ha) are currently only available in Garbsen

(14 ha), Uetze (14 ha) and in the state capital of Hanover (11 ha). - Land reserves with legally binding B-plans (available either immediately or later) of more than 10 ha are located in Uetze (41 ha), Pattensen (24 ha), Springe (21 ha), the state capital (19 ha), Garbsen (18 ha), Burgwedel (16 ha), Lehrte, Sehnde and Burgdorf (12 ha each).

- F-plan reserves (without a legally binding B-plan) of more than 20 ha are located in Lehrte (115 ha), Barsinghausen (59 ha), Uetze (53 ha), Springe (45 ha), Sehnde (37 ha), Neustadt (36 ha) and Garbsen (29 ha).

Looking at the development of commercial space potential compared to the previous year, it can be seen that two municipalities recorded a significant increase (> + 2 ha) in the potential supply of space.

- Uetze: With an increase in land potential of 25.6 ha, Uetze recorded the strongest increase in land supply. The increase is due to the expansion of the plans for the Dollbergen-Gasolin industrial estate by 20 ha and the new registration of the Uetze-Nordost industrial estate, which contributes 5.6 ha to the land balance.

- Springe: The amount of available space increased by 4.7 ha due to two expansions of existing industrial estates. The area available in the Springe/Osttangente industrial estate has increased by 4.4 ha, while the area in the Bennigsen/Schildbruch industrial estate has increased by 0.3 ha.

Potentially reusable brownfield sites

It is not only in conurbations such as the Hannover Region that the development options for new greenfield commercial sites are increasingly reaching their limits due to competition for land and requirements for open space protection. For this reason, the revitalization of brownfield sites, the careful use of land resources and the densification of use in existing commercial areas are among the central objectives of municipal commercial space policy.

In this context, brownfield sites are defined as areas formerly used for commercial purposes that are fundamentally suitable for commercial reuse, but cannot be mobilized via market mechanisms due to significant obstacles to use such as contaminated sites, old buildings or planning restrictions and therefore trigger a need for public action. An indication of significant restrictions on use is a longer vacancy period than is usual on the market. A significant size of the property is also a prerequisite for the need for public action.

As part of the commercial space monitoring, 14 properties with 86 ha are recorded according to this definition, which are listed in the following table in alphabetical order of the surrounding municipalities and the state capital Hannover (Table 3).

Available space in the Hannover Region